Geopolitics, UK Autumn budget & US data in focus

- US markets closed on Thursday for Thanksgiving holiday

- UK budget could rock British Pound on Wednesday

- US data likely to impact Fed cut bets for December

- Bitcoin still shaky while gold searches for direction

Despite the shortened holiday week, November could end with a bang due to a lineup of high-impact events.

Equity markets have already kicked off on a positive note with tech leading gains amid rising expectations for a December US rate cut. A string of dovish messages by Fed officials last Friday boosted these odds to 70% but incoming US data may either reinforce or shave these bets.

Over the weekend, US top diplomats met with Ukrainian and European officials to discuss a Russia-Ukraine peace plan. However, European leaders have rejected such plans, with US and Ukraine promising an “updated and refined framework”. Should talks end in a deadlock, this could spark risk aversion across the board.

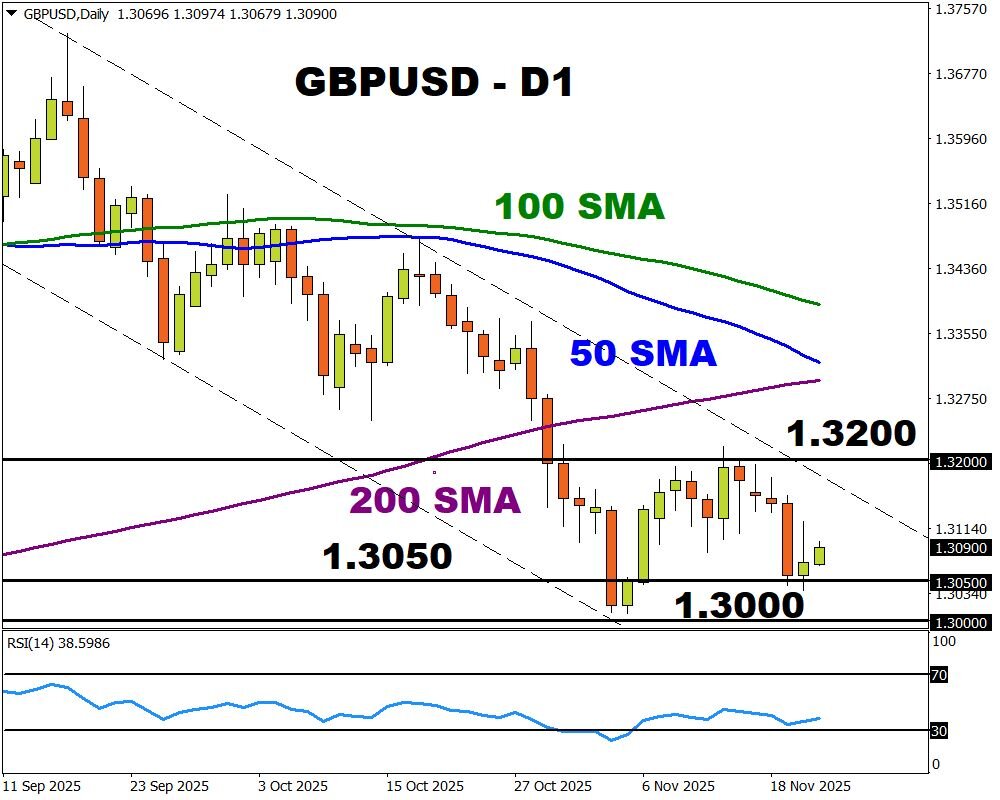

GBPUSD could be set for a week of mayhem due to the pivotal UK Autumn budget on Wednesday, 26th November. With the UK fiscal hole as much as £30 billion, tax hikes are expected, potentially leading to more pain for consumers with a drop in disposable incoming, hitting growth. If this raises bets around lower UK rates, the Pound could be in for fresh pain.

In the United States, incoming US retail sales and PPI may provide more insight into the health of the economy. Should data disappoint, this may fuel bets around the Fed cutting rates in December.

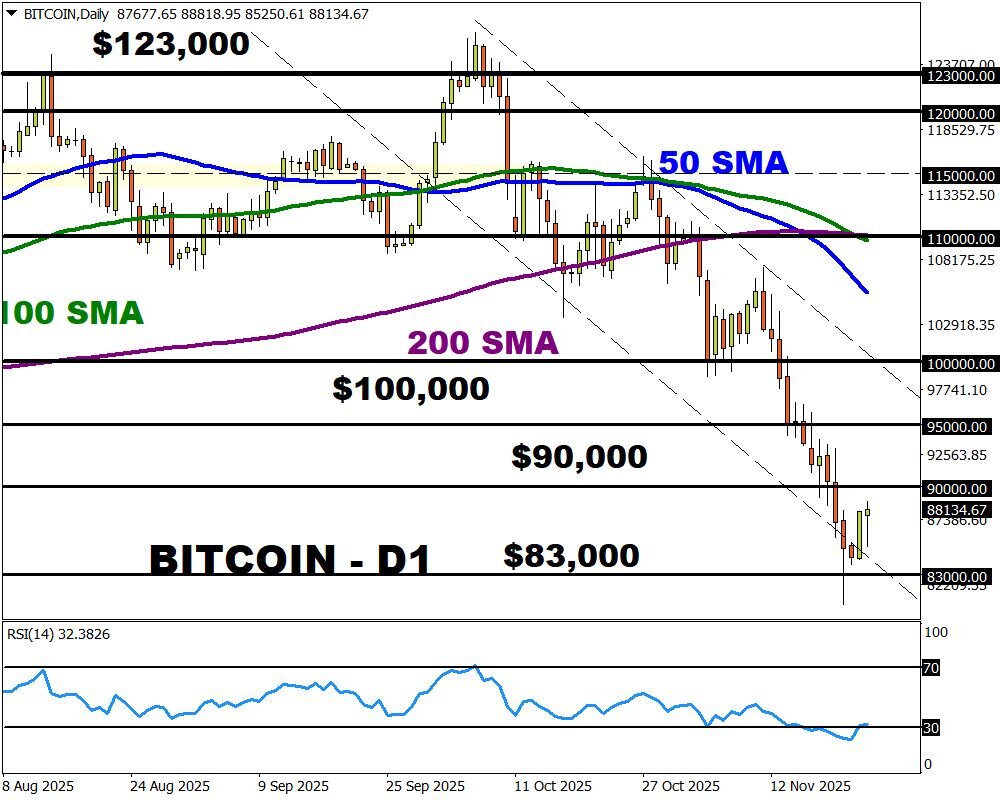

Focusing on cryptos, Bitcoin struggled to nurse the deep wounds inflicted from last week’s brutal selloff. Despite the recent rebound, prices are on track for their worst month since 2022 with prices down nearly 10% year-to-date. Bitcoin is wobbling around $86,000 as of writing. Persistent weakness below $90,000 signalling a selloff toward $80,500 and lower.

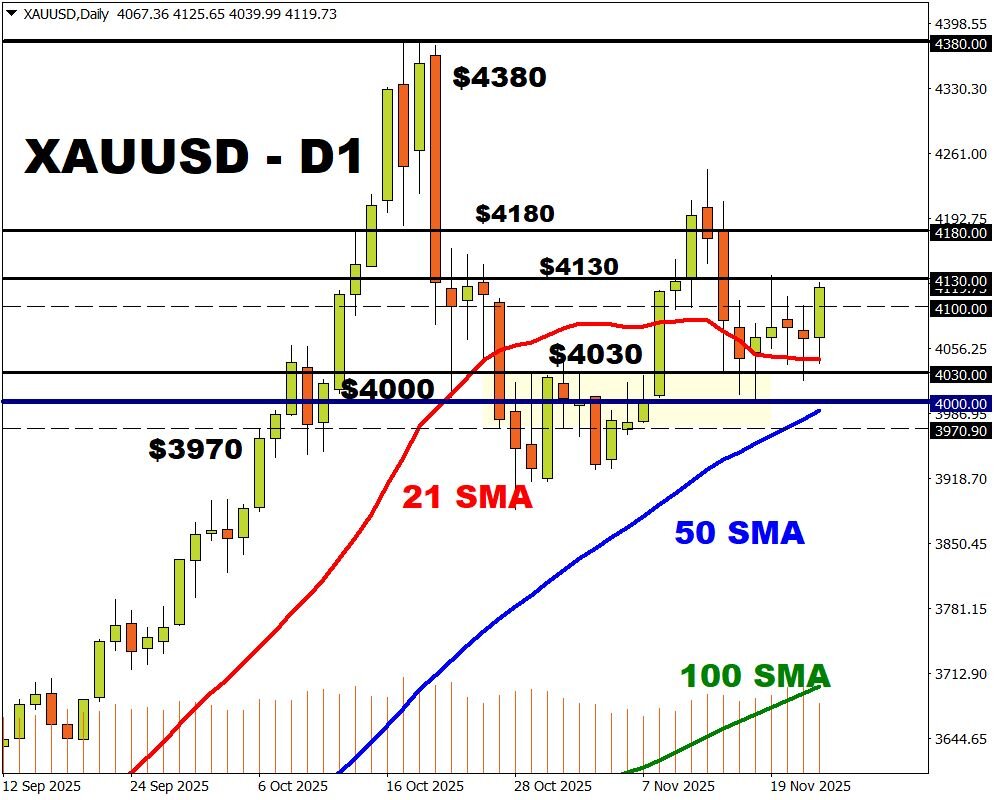

Looking at commodities, oil flashed red amid hopes about a Ukraine-Russia peace deal, while gold has been stuck within a wide range since mid-November. A potent fundamental catalyst may be needed to trigger a break above $4130 or below $4000. This may come in the form of geopolitical developments or key US data.